AIC 와 BIC 계산

통계모형을 선택하는 척도로서 가능도함수이론에 근거한 AIC(Akaike information criteria, 식 6.9 )와 베이지안 검정이론에 기초한 BIC(bayesian or schwartz information criteria, 식 6.8 )가 있으며 정의는 모형의 선택에 대한 절에 나타니 있다.

AIC 와 BIC 는 함수 AIC 와 BIC 를 이용하면 구할 수 있다.

<- lm (price ~ ., data= houseprice)

Call:

lm(formula = price ~ ., data = houseprice)

Coefficients:

(Intercept) tax ground floor year

1.21874 0.05195 0.01159 0.34941 -0.21894

위의 AIC 와 BIC 에서 로그 가능도 함수 \(\ell(\hat {\pmb \theta})\) 는 함수 logLik 로 구할 수 있다.

참고로 선형모형에 대한 AIC 와 BIC 는 식 6.10 에 의하여 다음과 같이 계산할 수 있다.

\[

\begin{aligned}

AIC &= n\log(2\pi) + n + n \log \frac{SSE_p}{n} + 2(p+1) \\

BIC &= n\log(2\pi) + n + n \log \frac{SSE_p}{n} + (\log n) (p+1)

\end{aligned}

\]

이제 회귀모형을 적합한 결과과 식 6.10 를 이용하여 직접 AIC 와 BIC 를 계산해보자.

<- dim (houseprice)[1 ]<- length (coef (fit1))<- deviance (fit1)c (n,p,sse)

[1] 27.00000 5.00000 91.44876

<- - 2 * logLik (fit1) + 2 * (p+ 1 )<- - 2 * logLik (fit1) + log (n)* (p+ 1 ) c (aic1, bic1)<- n* log (2 * pi) + n + n* log (deviance (fit1)/ n) + 2 * (p+ 1 ) <- n* log (2 * pi) + n + n* log (deviance (fit1)/ n) + log (n)* (p+ 1 )c (aic2, bic2)

예제 6.1

변수선택의 통계량

패키지 leaps 에 수록된 regsubsets() 함수를 이용하면 가능한 모든 모형에 대한 중요한 선택 기준들이 게산된다.

rss: 잔차 제곱합rsq: \(R^2\) adjr2 : 수정된 \(R^2\) cp : 맬로우의 \(C_p\) bic : BIC

교재 예제에 나타난 자료 houseprice는 독립변수의 수가 4개이므로 가능한 회귀식의 개수가 \(2^4=16\) 개이므로 이러한 방법을 적용할 수 있다. 하지만 독립변수의 수가 10개만 되면 가능한 회귀식의 수가 1024개나 되고 20개가 모형의 수가 100만개가 넘으므로 이들 모두에 대한 통계량을 계산하는 것은 실제로 쉽지않다.

이제 예제 자료 houseprice에 대하여 regsubsets함수를 사용하여 가능한 회귀식을 모두 적합하고 각 식에 대한 모형선택의 기준값을 계산해보자. regsubsets함수에서 nbest=6는 독립변수의 수가 같은 모형들 중에서 가장 좋은 6개의 모형만을 보여주라는 명령문이다.

모든 가능한 회귀식에 대한 통계량은 summaryf함수를 통하여 볼 수 있다.

<- regsubsets (price ~ . , data= houseprice, nbest= 6 )summaryf (houseprice.rgs)

tax ground floor year rss rsq adjr2 cp

1 ( 1 ) * 182.66315 0.86271916 0.85722792 20.943616

1 ( 2 ) * 215.97764 0.83768158 0.83118885 28.958146

1 ( 3 ) * 628.61671 0.52756188 0.50866435 128.227503

1 ( 4 ) * 1202.47186 0.09627993 0.06013112 266.280912

2 ( 1 ) * * 95.19550 0.92845564 0.92249361 1.901360

2 ( 2 ) * * 153.80917 0.88440442 0.87477146 16.002160

2 ( 3 ) * * 168.58785 0.87329747 0.86273892 19.557496

2 ( 4 ) * * 191.93607 0.85575007 0.84372925 25.174420

2 ( 5 ) * * 214.64151 0.83868576 0.82524290 30.636710

2 ( 6 ) * * 626.80968 0.52891996 0.48966329 129.792782

3 ( 1 ) * * * 92.31936 0.93061720 0.92156727 3.209442

3 ( 2 ) * * * 93.26197 0.92990878 0.92076645 3.436208

3 ( 3 ) * * * 150.10029 0.88719183 0.87247773 17.109908

3 ( 4 ) * * * 187.51305 0.85907420 0.84069258 26.110366

4 ( 1 ) * * * * 91.44876 0.93127151 0.91877542 5.000000

bic

1 ( 1 ) -47.022941

1 ( 2 ) -42.499601

1 ( 3 ) -13.654236

1 ( 4 ) 3.858312

2 ( 1 ) -61.323304

2 ( 2 ) -48.369244

2 ( 3 ) -45.892146

2 ( 4 ) -42.390102

2 ( 5 ) -39.371316

2 ( 6 ) -10.436125

3 ( 1 ) -58.855794

3 ( 2 ) -58.581513

3 ( 3 ) -45.732450

3 ( 4 ) -39.723741

4 ( 1 ) -55.815783

위의 결과를 보면 두 개의 변수 tax와 floor가 포함된 회귀식이 다음과 같은 통계량으로 가장 좋은 모형으로 나타난다.

rss: 잔차제곱합(residual sum of square), \(SSE = 95.20\) rsq: 결정계수(\(R^2_p\) ), \(R^2=0.92846\) adjr2: 수정된 결정계수(\(R^2_{ap}\) ), \(R^2_a=0.92249\) cp: 맬로우즈 \(C_p\) , \(C_p = 1.901\) bic: BIC(Bayesian Information Criteria), \(BIC= -61.323\)

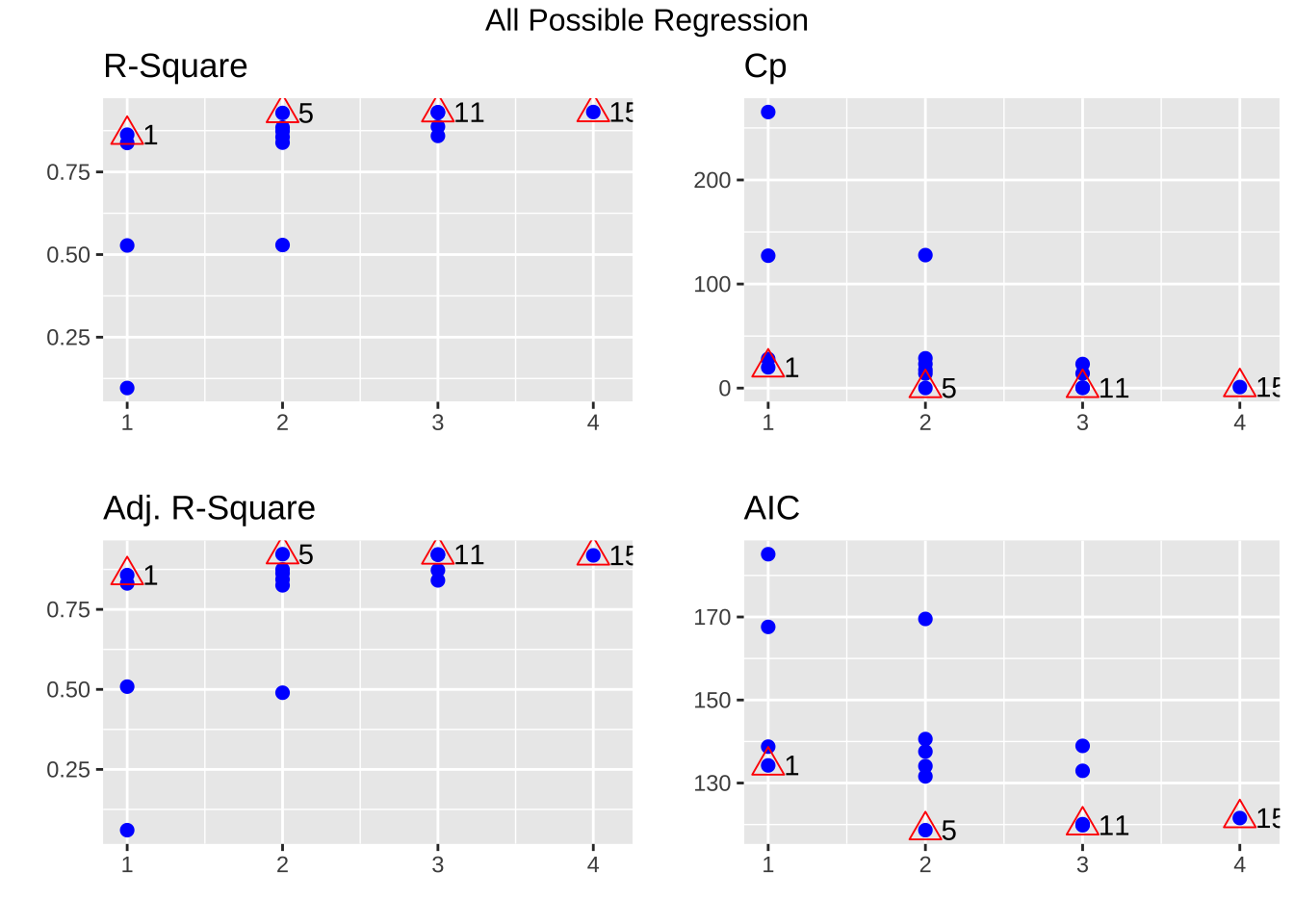

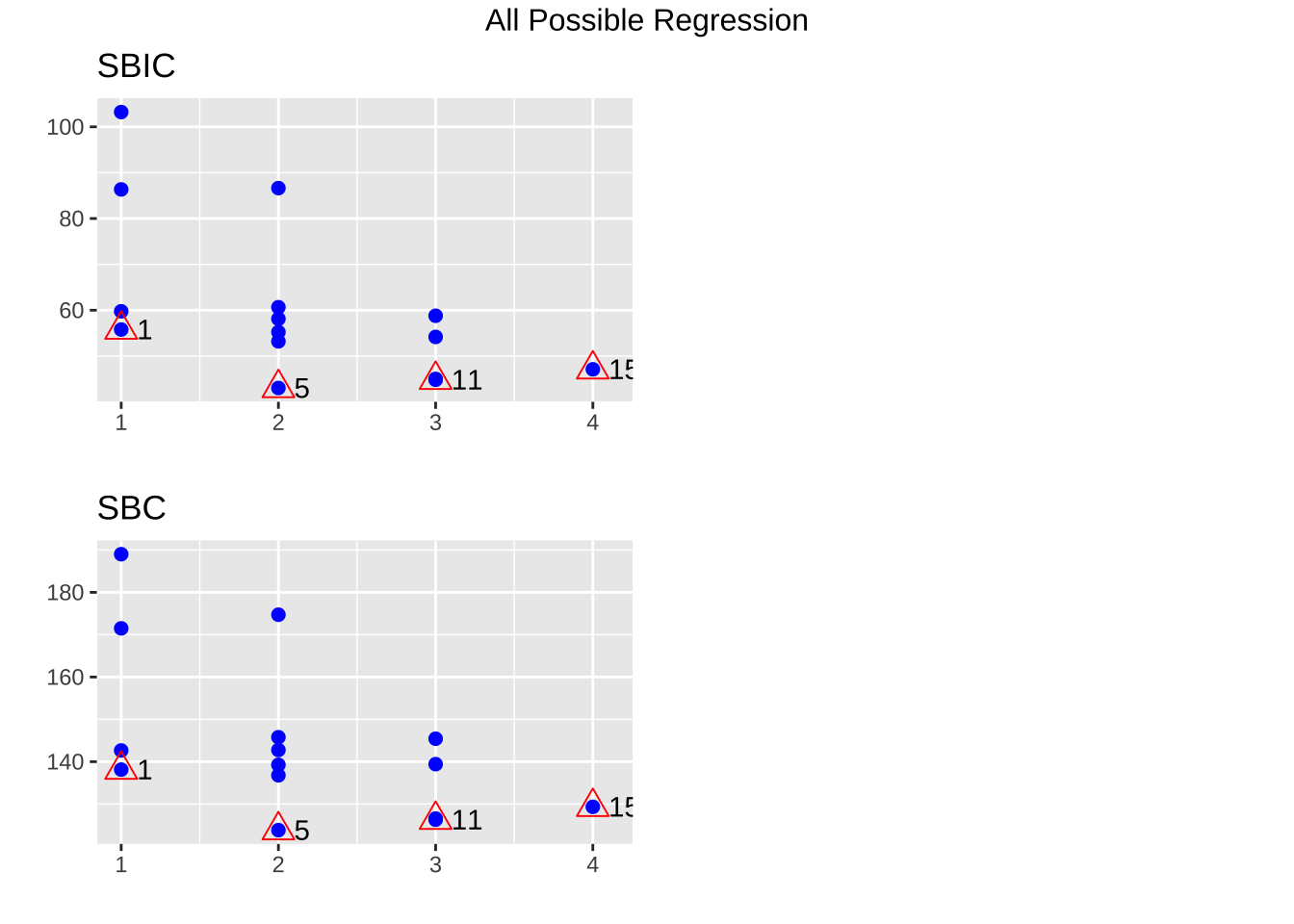

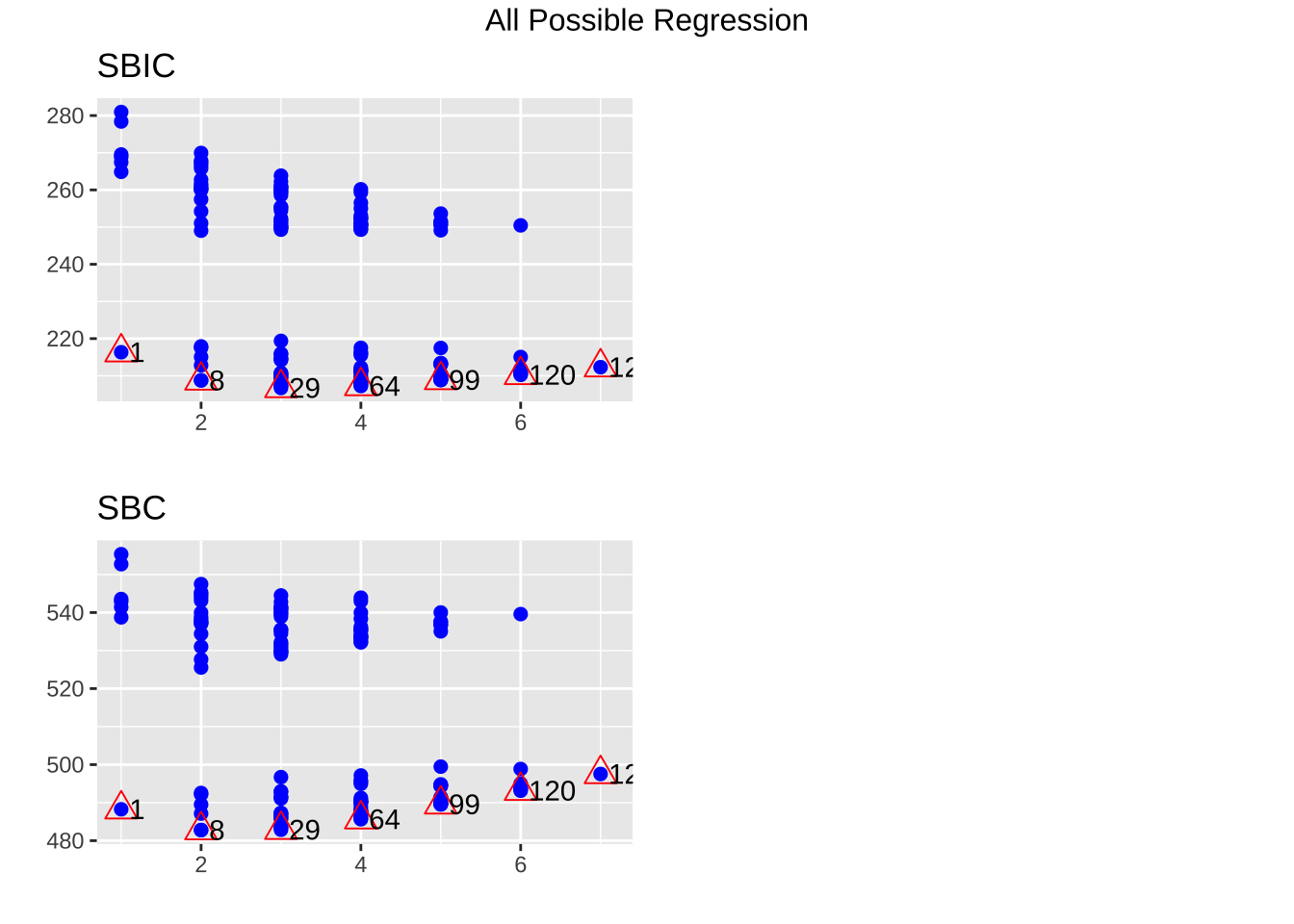

패키지 olsrr에 있는 함수 ols_step_all_possible()을 이용하면 가능한 모든 회귀모형에 대한 통계량을 구하고 여러 가지 통계량에 대한 그림을 plot() 함수를 이용하여 쉽게 그릴 수 있다.

<- lm (price ~ ., data= houseprice)<- ols_step_all_possible (fit1)

Index N Predictors R-Square Adj. R-Square Mallow's Cp

3 1 1 floor 0.86271916 0.85722792 20.943616

1 2 1 tax 0.83768158 0.83118885 28.958146

2 3 1 ground 0.52756188 0.50866435 128.227503

4 4 1 year 0.09627993 0.06013112 266.280912

6 5 2 tax floor 0.92845564 0.92249361 1.901360

10 6 2 floor year 0.88440442 0.87477146 16.002160

8 7 2 ground floor 0.87329747 0.86273892 19.557496

5 8 2 tax ground 0.85575007 0.84372925 25.174420

7 9 2 tax year 0.83868576 0.82524290 30.636710

9 10 2 ground year 0.52891996 0.48966329 129.792782

13 11 3 tax floor year 0.93061720 0.92156727 3.209442

11 12 3 tax ground floor 0.92990878 0.92076645 3.436208

14 13 3 ground floor year 0.88719183 0.87247773 17.109908

12 14 3 tax ground year 0.85907420 0.84069258 26.110366

15 15 4 tax ground floor year 0.93127151 0.91877542 5.000000

$ result %>% dplyr:: select (mindex, n, predictors, rsquare, adjr, cp, aic, sbc) %>% dplyr:: arrange (sbc)

mindex n predictors rsquare adjr cp aic

1 5 2 tax floor 0.92845564 0.92249361 1.901360 118.6453

2 11 3 tax floor year 0.93061720 0.92156727 3.209442 119.8169

3 12 3 tax ground floor 0.92990878 0.92076645 3.436208 120.0912

4 15 4 tax ground floor year 0.93127151 0.91877542 5.000000 121.5611

5 6 2 floor year 0.88440442 0.87477146 16.002160 131.5993

6 1 1 floor 0.86271916 0.85722792 20.943616 134.2415

7 7 2 ground floor 0.87329747 0.86273892 19.557496 134.0764

8 13 3 ground floor year 0.88719183 0.87247773 17.109908 132.9403

9 2 1 tax 0.83768158 0.83118885 28.958146 138.7648

10 8 2 tax ground 0.85575007 0.84372925 25.174420 137.5785

11 14 3 tax ground year 0.85907420 0.84069258 26.110366 138.9490

12 9 2 tax year 0.83868576 0.82524290 30.636710 140.5973

13 3 1 ground 0.52756188 0.50866435 128.227503 167.6102

14 10 2 ground year 0.52891996 0.48966329 129.792782 169.5324

15 4 1 year 0.09627993 0.06013112 266.280912 185.1227

sbc

1 123.8286

2 126.2961

3 126.5704

4 129.3361

5 136.7827

6 138.1290

7 139.2598

8 139.4195

9 142.6523

10 142.7618

11 145.4282

12 145.7806

13 171.4977

14 174.7158

15 189.0102

PRESS 잔차는 함수 press() 로 구할 수 있다.

\[ \text{PRESS}_p = \sum_{i=1}^n ( y_i - \hat y_{i(i)})^2 \]

또한 교과서 264 페이지에 나온 교차확인(cross validation)에 의거한 \(R^2_{pred}\) 은 다음과 같이 계산되며 press() 함수에 의해 주어진다.

\[ R^2_{pred} = 1 - \frac{ \text{PRESS}_p}{\text{SST}} \]

tax ground floor year PRESS pred.r.squared

1 ( 1 ) * 220.8853 0.8339932

1 ( 2 ) * 316.0868 0.7624443

1 ( 3 ) * 838.8121 0.3695891

1 ( 4 ) * 1430.6084 0.0000000

2 ( 1 ) * * 144.3991 0.8914766

2 ( 2 ) * * 207.6594 0.8439331

2 ( 3 ) * * 233.7615 0.8243161

2 ( 4 ) * * 358.2145 0.7307832

2 ( 5 ) * * 341.4294 0.7433981

2 ( 6 ) * * 911.3553 0.3150691

3 ( 1 ) * * * 153.5941 0.8845661

3 ( 2 ) * * * 159.1752 0.8803716

3 ( 3 ) * * * 233.2240 0.8247200

3 ( 4 ) * * * 380.1744 0.7142792

4 ( 1 ) * * * * 170.4810 0.8718747

이상치를 제거한 경우

교과서에서 분석하였듯이 9,10,27 번째 자료가 이상점 또는 영향점일 가능성이 높으므로 이를 제거하고 모형의 선택 기준을 다시 계산해 보자.

<- houseprice[- c (9 ,10 ,27 ),]<- lm (price ~ . , data= housepriceEX)summary (housepriceEX.lm)

Call:

lm(formula = price ~ ., data = housepriceEX)

Residuals:

Min 1Q Median 3Q Max

-2.4130 -1.0459 -0.2558 0.8593 2.8197

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.32538 2.14531 2.948 0.00825 **

tax 0.06589 0.01874 3.516 0.00231 **

ground 0.00974 0.02168 0.449 0.65835

floor 0.08578 0.09057 0.947 0.35547

year -0.11142 0.26781 -0.416 0.68205

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.543 on 19 degrees of freedom

Multiple R-squared: 0.7819, Adjusted R-squared: 0.7359

F-statistic: 17.02 on 4 and 19 DF, p-value: 4.404e-06

이상치를 제거하면 tax 만 포함된 모형이 최적모형으로 나타난다. 이상치와 영항점이 모형의 선택에도 영향을 주는 점에 꼭 유의하자.

<- regsubsets (price ~ . , data= housepriceEX, nbest= 6 )summaryf (housepriceEX.rgs)

tax ground floor year rss rsq adjr2 cp

1 ( 1 ) * 48.17790 0.7675502 0.7569843 0.2458362

1 ( 2 ) * 102.73566 0.5043188 0.4817878 23.1726808

1 ( 3 ) * 125.87070 0.3926964 0.3650917 32.8947363

1 ( 4 ) * 174.34503 0.1588164 0.1205808 53.2651405

2 ( 1 ) * * 46.18667 0.7771576 0.7559345 1.4090560

2 ( 2 ) * * 47.39011 0.7713512 0.7495751 1.9147822

2 ( 3 ) * * 48.11577 0.7678500 0.7457405 2.2197243

2 ( 4 ) * * 83.74651 0.5959380 0.5574559 17.1928590

2 ( 5 ) * * 85.27968 0.5885408 0.5493542 17.8371405

2 ( 6 ) * * 116.96847 0.4356480 0.3819002 31.1537464

3 ( 1 ) * * * 45.62514 0.7798669 0.7468469 3.1730851

3 ( 2 ) * * * 45.69348 0.7795371 0.7464677 3.2018056

3 ( 3 ) * * * 47.34784 0.7715551 0.7372884 3.8970174

3 ( 4 ) * * * 74.63053 0.6399210 0.5859092 15.3620431

4 ( 1 ) * * * * 45.21326 0.7818541 0.7359287 5.0000000

bic

1 ( 1 ) -28.661838

1 ( 2 ) -10.487628

1 ( 3 ) -5.613326

1 ( 4 ) 2.205420

2 ( 1 ) -26.496810

2 ( 2 ) -25.879469

2 ( 3 ) -25.514758

2 ( 4 ) -12.214327

2 ( 5 ) -11.778929

2 ( 6 ) -4.195690

3 ( 1 ) -23.612331

3 ( 2 ) -23.576407

3 ( 3 ) -22.722834

3 ( 4 ) -11.802150

4 ( 1 ) -20.651921

<- ols_step_all_possible (lm (price ~ ., data= housepriceEX))$ result %>% as.data.frame () %>% dplyr:: select (mindex, n, predictors, rsquare, adjr, cp, aic, sbc) %>% dplyr:: arrange (sbc)

mindex n predictors rsquare adjr cp aic

1 1 1 tax 0.7675502 0.7569843 0.2458362 90.83337

2 5 2 tax floor 0.7771576 0.7559345 1.4090560 91.82034

3 6 2 tax ground 0.7713512 0.7495751 1.9147822 92.43768

4 7 2 tax year 0.7678500 0.7457405 2.2197243 92.80240

5 11 3 tax ground floor 0.7798669 0.7468469 3.1730851 93.52677

6 12 3 tax floor year 0.7795371 0.7464677 3.2018056 93.56269

7 13 3 tax ground year 0.7715551 0.7372884 3.8970174 94.41627

8 15 4 tax ground floor year 0.7818541 0.7359287 5.0000000 95.30913

9 8 2 floor year 0.5959380 0.5574559 17.1928590 106.10283

10 14 3 ground floor year 0.6399210 0.5859092 15.3620431 105.33695

11 9 2 ground floor 0.5885408 0.5493542 17.8371405 106.53823

12 2 1 floor 0.5043188 0.4817878 23.1726808 109.00758

13 3 1 ground 0.3926964 0.3650917 32.8947363 113.88188

14 10 2 ground year 0.4356480 0.3819002 31.1537464 114.12146

15 4 1 year 0.1588164 0.1205808 53.2651405 121.70063

sbc

1 94.36753

2 96.53256

3 97.14990

4 97.51461

5 99.41704

6 99.45296

7 100.30654

8 102.37745

9 110.81504

10 111.22722

11 111.25044

12 112.54174

13 117.41604

14 118.83368

15 125.23479

tax ground floor year PRESS pred.r.squared

1 ( 1 ) * 56.10399 0.72930829

1 ( 2 ) * 117.36430 0.43373824

1 ( 3 ) * 157.83378 0.23848023

1 ( 4 ) * 202.40162 0.02344834

2 ( 1 ) * * 57.66354 0.72178375

2 ( 2 ) * * 64.24819 0.69001399

2 ( 3 ) * * 63.42708 0.69397570

2 ( 4 ) * * 108.09369 0.47846724

2 ( 5 ) * * 114.27185 0.44865875

2 ( 6 ) * * 160.37982 0.22619605

3 ( 1 ) * * * 68.98320 0.66716837

3 ( 2 ) * * * 65.44694 0.68423019

3 ( 3 ) * * * 72.26745 0.65132247

3 ( 4 ) * * * 109.76504 0.47040332

4 ( 1 ) * * * * 79.24660 0.61764930

변수선택 방법

회귀식에서 변수를을 선택할 때 가장 큰 모형을 적합시키면 각 변수에 대한 중요도를 각 회귀계수에 대한 가설 검정 \(H_o: \beta_i=0\) 에 대한 t-통계량을 보고 판단할 수 있다.

다시 모든 자료를 고려한 houseprice에 대하여 가장 큰 모형을 적합시킨 후 각 변수에 대한 t-검정을 실시해보자.

Call:

lm(formula = price ~ ., data = houseprice)

Residuals:

Min 1Q Median 3Q Max

-3.4891 -1.3574 0.1337 1.0686 3.4938

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.21874 2.04661 0.595 0.55759

tax 0.05195 0.01383 3.756 0.00109 **

ground 0.01159 0.02534 0.458 0.65169

floor 0.34941 0.07268 4.807 8.41e-05 ***

year -0.21894 0.33149 -0.660 0.51582

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.039 on 22 degrees of freedom

Multiple R-squared: 0.9313, Adjusted R-squared: 0.9188

F-statistic: 74.53 on 4 and 22 DF, p-value: 1.817e-12

위는 4개의 독립변수를 포함한 가장 큰 모형에 대하여 각 계수의 유의성 검정에 대한 결과이다. 변수 floor가 가장 유의한 변수이고 다음으로 tax가 유의함을 알 수 있다. 또한 2개의 변수 year와 ground는 유의하지 않음을 알 수 있다.

이렇게 독립변수들은 반응변수를 설명하는 정도가 다르므로 모든 가능한 회귀식을 적합하여 모형을 선택하는 것보다 변수의 중요도를 고려하여 변수들을 유의한 정도에 따라 차례로 모형에 포함시키거나 제거하는 절차가 더 효율적이다. 이렇게 가장 단순한 모형(평균모형)에서 시작하여 설명력이 높은 변수들을 순차적으로 포함시키거나(forward selection; 전진선택) 가장 큰 모형(full model)에서 시작하여 설명력이 낮은 변수들을 차례로 제거하는 방법(backward elimination; 후방제거)을 단계별 회귀(stepwise regression)이라고 한다.

단계별 회귀는 다음과 같은 세 가지 방법이 있다.

전진선택 (forward selection)

후방제거 (backward elimination)

단계별 선택 (stepwise selection)

단계별 선택은 전진선택과 후방제거를 결합한 형태로서 새로운 변수가 추가되는 경우마다(전진선택) 제거할 변수를 있는지 판단하여 유의하지 않다면 제거하는(후방제거) 방법이다.

단계별 선택의 적용

단계별 선택에서 전진선택과 후방제거는 add1()와 drop1()함수를 사용한다.

평균모형

\[ y=\beta_0 + \epsilon \]

<- lm (price~ 1 , houseprice)summary (model0)

Call:

lm(formula = price ~ 1, data = houseprice)

Residuals:

Min 1Q Median 3Q Max

-6.300 -4.275 -0.800 1.125 23.200

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 19.250 1.377 13.98 1.32e-13 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 7.154 on 26 degrees of freedom

첫번째 변수의 추가

이제 가장 설명력있는 변수를 추가하는데 다음과 같은 2개의 모형을 비교하는 부분 F 검정을 이용하여 가장 유의한 변수를 추가한다.

\[ H_0: y=\beta_0 + \epsilon \quad \text{vs} \quad H_1: y=\beta_0 + \beta_1 x_i + \epsilon \]

add1 (model0, scope= ~ tax+ ground+ floor+ year, test= "F" )

Single term additions

Model:

price ~ 1

Df Sum of Sq RSS AIC F value Pr(>F)

<none> 1330.58 107.233

tax 1 1114.60 215.98 60.142 129.0183 2.310e-11 ***

ground 1 701.96 628.62 88.987 27.9170 1.792e-05 ***

floor 1 1147.92 182.66 55.619 157.1084 2.807e-12 ***

year 1 128.11 1202.47 106.500 2.6634 0.1152

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

위의 결과에서 가장 유의한 변수가 floor이므로 회귀식에 추가한다. 변수를 추가하는 경우는 고려하는 변수를 포함한 모형과 포함하지 않는 모형이 가장 유의한 차이를 보이는 변수를 선택한다.

<- update (model0, . ~ . + floor)summary (model1)

Call:

lm(formula = price ~ floor, data = houseprice)

Residuals:

Min 1Q Median 3Q Max

-4.6682 -2.1916 -0.1459 2.0517 4.9644

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.25296 1.52716 0.82 0.42

floor 0.59511 0.04748 12.53 2.81e-12 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.703 on 25 degrees of freedom

Multiple R-squared: 0.8627, Adjusted R-squared: 0.8572

F-statistic: 157.1 on 1 and 25 DF, p-value: 2.807e-12

위에서 update() 함수는 앞에서 적합한 모형 model0에 변수 floor를 추가한다.

두 번째 변수의 추가

add1 (model1, scope= ~ tax+ ground+ floor+ year, test= "F" )

Single term additions

Model:

price ~ floor

Df Sum of Sq RSS AIC F value Pr(>F)

<none> 182.663 55.619

tax 1 87.468 95.195 40.023 22.0517 8.997e-05 ***

ground 1 14.075 168.588 55.454 2.0037 0.16976

year 1 28.854 153.809 52.977 4.5023 0.04437 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

<- update (model1, . ~ . + tax)summary (model2)

Call:

lm(formula = price ~ floor + tax, data = houseprice)

Residuals:

Min 1Q Median 3Q Max

-3.009 -1.658 0.048 1.220 3.548

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.39497 1.13994 0.346 0.732

floor 0.34835 0.06313 5.518 1.13e-05 ***

tax 0.05742 0.01223 4.696 9.00e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.992 on 24 degrees of freedom

Multiple R-squared: 0.9285, Adjusted R-squared: 0.9225

F-statistic: 155.7 on 2 and 24 DF, p-value: 1.798e-14

위의 결과로부터 변수 tax가 가장 유의한 변수임을 알 수 있고 이를 모형에 추가한다.

변수의 제거

이제 독립변수가 두 개가(floor와 tax) 모형에 포함되었고 가장 최근에 포함된 변수 tax를 제외한 나머지 변수를 제거할 수 있는지 감정한다. 후방제거하는 경우는 제거할 변수가 포함된 모형과 포함하지 않는 모형의 설명력에 유의한 차이가 없어야 한다. 즉 F-검정이 유의하니 않으면 제거한다.

Single term deletions

Model:

price ~ floor + tax

Df Sum of Sq RSS AIC F value Pr(>F)

<none> 95.195 40.023

floor 1 120.782 215.978 60.142 30.451 1.126e-05 ***

tax 1 87.468 182.663 55.619 22.052 8.997e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

위의 함수 drop1()의 결과에서 모든 변수에 대한 F-통계량이 유의하므로 변수를 제거하지 않는다.

세 번째 변수의 추가

독립변수가 두 개가(floor와 tax) 모형에 새로운 변수를 추가하는 검정을 실시해 보자

add1 (model2, scope= ~ tax+ ground+ floor+ year, test= "F" )

Single term additions

Model:

price ~ floor + tax

Df Sum of Sq RSS AIC F value Pr(>F)

<none> 95.195 40.023

ground 1 1.9335 93.262 41.469 0.4768 0.4968

year 1 2.8761 92.319 41.194 0.7165 0.4060

위의 결과에서 유의한 변수가 없으므로 더 이상 변수를 추가하지 않는다.

최종 모형

더 이상 추가할 변수와 제거할 변수가 없으면 단계별 선택을 중단한다. 따라서 단계별 선택법에 의한 최종 모형은 floor와 tax, 두 개의 독립변수를 포함하는 모형이다.

이러한 단계별 회귀의 결과는 모든 가능한 회귀에 의한 방법과 모형이 일치한다. 독립변수의 수가 많는 경우 이러한 단계별 회귀 방법은 유용하게 사용된다.

함수 step()

위에서 논의한 세 종류의 변수선택법은 함수 step()을 이용하여 한 번에 결과를 얻을 수 있다.

주의할 점은 함수 step()은 변수의 선택 기준이 F-검정이 아니 AIC 를 이용한다는 점이다.

<- lm (price~ 1 , houseprice)step (model0, scope= ~ tax+ ground+ floor+ year, direction= "forward" )

Start: AIC=107.23

price ~ 1

Df Sum of Sq RSS AIC

+ floor 1 1147.92 182.66 55.619

+ tax 1 1114.60 215.98 60.142

+ ground 1 701.96 628.62 88.987

+ year 1 128.11 1202.47 106.500

<none> 1330.58 107.233

Step: AIC=55.62

price ~ floor

Df Sum of Sq RSS AIC

+ tax 1 87.468 95.195 40.023

+ year 1 28.854 153.809 52.977

+ ground 1 14.075 168.588 55.454

<none> 182.663 55.619

Step: AIC=40.02

price ~ floor + tax

Df Sum of Sq RSS AIC

<none> 95.195 40.023

+ year 1 2.8761 92.319 41.194

+ ground 1 1.9335 93.262 41.469

Call:

lm(formula = price ~ floor + tax, data = houseprice)

Coefficients:

(Intercept) floor tax

0.39497 0.34835 0.05742

<- lm (price~ tax+ ground+ floor+ year, houseprice)step (fit, direction= "backward" )

Start: AIC=42.94

price ~ tax + ground + floor + year

Df Sum of Sq RSS AIC

- ground 1 0.871 92.319 41.194

- year 1 1.813 93.262 41.469

<none> 91.449 42.938

- tax 1 58.652 150.100 54.318

- floor 1 96.064 187.513 60.326

Step: AIC=41.19

price ~ tax + floor + year

Df Sum of Sq RSS AIC

- year 1 2.876 95.195 40.023

<none> 92.319 41.194

- tax 1 61.490 153.809 52.977

- floor 1 122.322 214.642 61.975

Step: AIC=40.02

price ~ tax + floor

Df Sum of Sq RSS AIC

<none> 95.195 40.023

- tax 1 87.468 182.663 55.619

- floor 1 120.782 215.978 60.142

Call:

lm(formula = price ~ tax + floor, data = houseprice)

Coefficients:

(Intercept) tax floor

0.39497 0.05742 0.34835

<- lm (price~ 1 , houseprice)step (model0, scope= ~ tax+ ground+ floor+ year, direction= "both" )

Start: AIC=107.23

price ~ 1

Df Sum of Sq RSS AIC

+ floor 1 1147.92 182.66 55.619

+ tax 1 1114.60 215.98 60.142

+ ground 1 701.96 628.62 88.987

+ year 1 128.11 1202.47 106.500

<none> 1330.58 107.233

Step: AIC=55.62

price ~ floor

Df Sum of Sq RSS AIC

+ tax 1 87.47 95.20 40.023

+ year 1 28.85 153.81 52.977

+ ground 1 14.08 168.59 55.454

<none> 182.66 55.619

- floor 1 1147.92 1330.58 107.233

Step: AIC=40.02

price ~ floor + tax

Df Sum of Sq RSS AIC

<none> 95.195 40.023

+ year 1 2.876 92.319 41.194

+ ground 1 1.934 93.262 41.469

- tax 1 87.468 182.663 55.619

- floor 1 120.782 215.978 60.142

Call:

lm(formula = price ~ floor + tax, data = houseprice)

Coefficients:

(Intercept) floor tax

0.39497 0.34835 0.05742

패키지 olsrr 의 이용

패키지 olsrr 의 함수 ols_step_both_p() 이용하여 F-검정을 이용한 단계별 선택을 할 수 있다.

함수 ols_step_both_p() 이용하여 F-검정에서는 유의수준을 지정해주지 않으면 유의 수준을 0.3 으로 사용한다.

참고로 SAS 의 모형 선택에서 자동적으로 사용되는 유의수준은 전진선택에서는 0.5, 후방제거에서는 0.1 이다.

ols_step_forward_p(model, penter = 0.3,

progress = FALSE, details = FALSE, ...)

ols_step_backward_p(model, prem = 0.3,

progress = FALSE, details = FALSE, ...)

Forward Selection (FORWARD)

The p-values for these F statistics are compared to the SLENTRY= value that is specified in the MODEL statement (or to 0.50 if the SLENTRY= option is omitted).

Backward Elimination (BACKWARD)

F statistics significant at the SLSTAY= level specified in the MODEL statement (or at the 0.10 level if the SLSTAY= option is omitted).

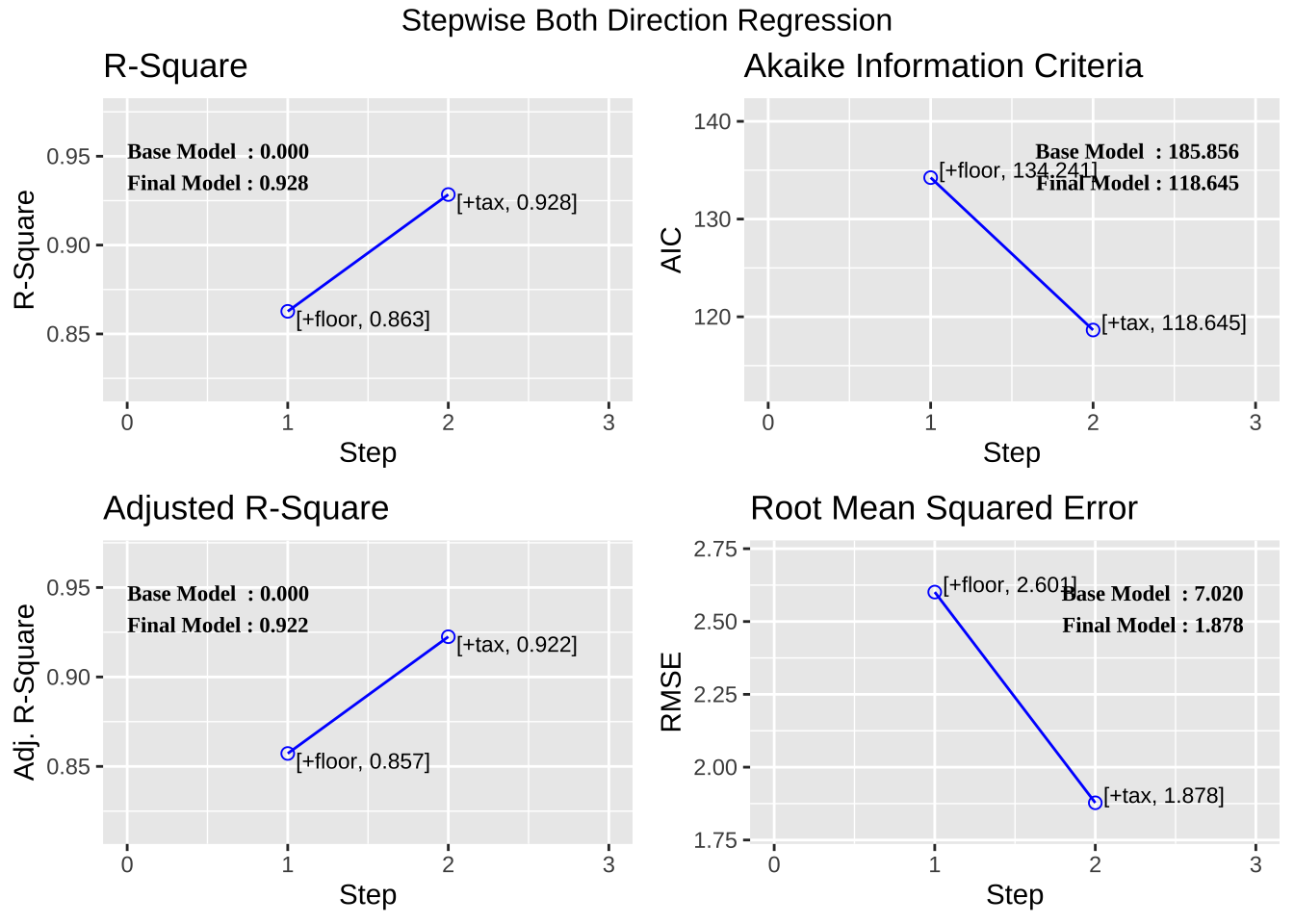

<- ols_step_both_p (fit1, details = TRUE )

Stepwise Selection Method

-------------------------

Candidate Terms:

1. tax

2. ground

3. floor

4. year

Step => 0

Model => price ~ 1

R2 => 0

Initiating stepwise selection...

Step => 1

Selected => floor

Model => price ~ floor

R2 => 0.863

Step => 2

Selected => tax

Model => price ~ floor + tax

R2 => 0.928

No more variables to be added or removed.

Stepwise Summary

-------------------------------------------------------------------------

Step Variable AIC SBC SBIC R2 Adj. R2

-------------------------------------------------------------------------

0 Base Model 185.856 188.448 105.725 0.00000 0.00000

1 floor (+) 134.241 138.129 55.779 0.86272 0.85723

2 tax (+) 118.645 123.829 43.032 0.92846 0.92249

-------------------------------------------------------------------------

Final Model Output

------------------

Model Summary

---------------------------------------------------------------

R 0.964 RMSE 1.878

R-Squared 0.928 MSE 3.526

Adj. R-Squared 0.922 Coef. Var 10.346

Pred R-Squared 0.891 AIC 118.645

MAE 1.572 SBC 123.829

---------------------------------------------------------------

RMSE: Root Mean Square Error

MSE: Mean Square Error

MAE: Mean Absolute Error

AIC: Akaike Information Criteria

SBC: Schwarz Bayesian Criteria

ANOVA

---------------------------------------------------------------------

Sum of

Squares DF Mean Square F Sig.

---------------------------------------------------------------------

Regression 1235.385 2 617.692 155.728 0.0000

Residual 95.195 24 3.966

Total 1330.580 26

---------------------------------------------------------------------

Parameter Estimates

-------------------------------------------------------------------------------------

model Beta Std. Error Std. Beta t Sig lower upper

-------------------------------------------------------------------------------------

(Intercept) 0.395 1.140 0.346 0.732 -1.958 2.748

floor 0.348 0.063 0.544 5.518 0.000 0.218 0.479

tax 0.057 0.012 0.463 4.696 0.000 0.032 0.083

-------------------------------------------------------------------------------------

함수 ols_step_both_aic() 는 함수 step() 과 동일하게 AIC 를 이용하여 변수선택을 한다.

ols_step_forward_aic (fit1)

Stepwise Summary

-------------------------------------------------------------------------

Step Variable AIC SBC SBIC R2 Adj. R2

-------------------------------------------------------------------------

0 Base Model 185.856 188.448 105.725 0.00000 0.00000

1 floor 134.241 138.129 55.779 0.86272 0.85723

2 tax 118.645 123.829 43.032 0.92846 0.92249

-------------------------------------------------------------------------

Final Model Output

------------------

Model Summary

---------------------------------------------------------------

R 0.964 RMSE 1.878

R-Squared 0.928 MSE 3.526

Adj. R-Squared 0.922 Coef. Var 10.346

Pred R-Squared 0.891 AIC 118.645

MAE 1.572 SBC 123.829

---------------------------------------------------------------

RMSE: Root Mean Square Error

MSE: Mean Square Error

MAE: Mean Absolute Error

AIC: Akaike Information Criteria

SBC: Schwarz Bayesian Criteria

ANOVA

---------------------------------------------------------------------

Sum of

Squares DF Mean Square F Sig.

---------------------------------------------------------------------

Regression 1235.385 2 617.692 155.728 0.0000

Residual 95.195 24 3.966

Total 1330.580 26

---------------------------------------------------------------------

Parameter Estimates

-------------------------------------------------------------------------------------

model Beta Std. Error Std. Beta t Sig lower upper

-------------------------------------------------------------------------------------

(Intercept) 0.395 1.140 0.346 0.732 -1.958 2.748

floor 0.348 0.063 0.544 5.518 0.000 0.218 0.479

tax 0.057 0.012 0.463 4.696 0.000 0.032 0.083

-------------------------------------------------------------------------------------

연습문제 6.10

자료 cars93은 1993년 미국에서 판매된 93가지 종류의 저동차에 대한 자료이다. 변수 MPG.highway를 반응변수로 하고 EngineSize, Weight, Price, Width, Length, Horsepower, Wheelbae 7개의 변수를 고려하여 가장 적합한 모형을 선택해보자.

<- Cars93[c ("MPG.highway" ,"EngineSize" , "Weight" , "Price" , "Width" , "Length" , "Horsepower" , "Wheelbase" )]head (dat93)

MPG.highway EngineSize Weight Price Width Length Horsepower Wheelbase

1 31 1.8 2705 15.9 68 177 140 102

2 25 3.2 3560 33.9 71 195 200 115

3 26 2.8 3375 29.1 67 180 172 102

4 26 2.8 3405 37.7 70 193 172 106

5 30 3.5 3640 30.0 69 186 208 109

6 31 2.2 2880 15.7 69 189 110 105

완전모형

<- lm (MPG.highway~ . , data= dat93)summary (carfit)

Call:

lm(formula = MPG.highway ~ ., data = dat93)

Residuals:

Min 1Q Median 3Q Max

-6.3952 -1.9678 -0.1942 1.4516 10.1313

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 21.119770 12.809426 1.649 0.1029

EngineSize 0.483792 0.698257 0.693 0.4903

Weight -0.012833 0.001726 -7.434 7.69e-11 ***

Price -0.047157 0.059498 -0.793 0.4302

Width 0.079770 0.228192 0.350 0.7275

Length 0.058766 0.043322 1.356 0.1785

Horsepower 0.013296 0.013443 0.989 0.3254

Wheelbase 0.277231 0.118027 2.349 0.0212 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.95 on 85 degrees of freedom

Multiple R-squared: 0.7172, Adjusted R-squared: 0.694

F-statistic: 30.8 on 7 and 85 DF, p-value: < 2.2e-16

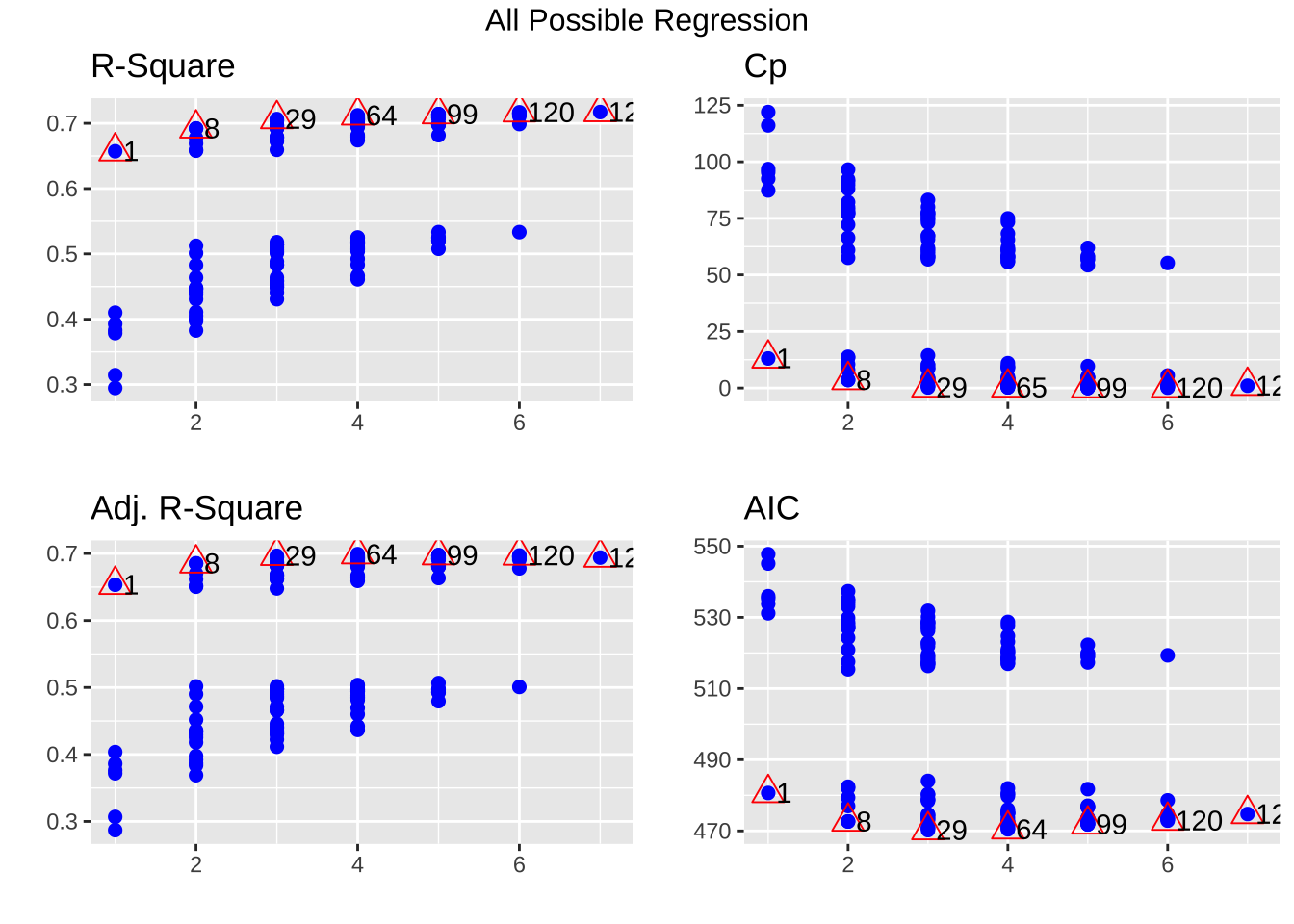

모든 가능한 회귀

<- ols_step_all_possible (carfit)$ result %>% dplyr:: select (mindex, n, predictors, rsquare, adjr, cp, aic, sbc) %>% :: arrange (sbc) %>% head (10 )

mindex n predictors rsquare adjr cp

1 8 2 Weight Length 0.6921969 0.6853568 5.527269

2 9 2 Weight Wheelbase 0.6920227 0.6851788 5.579611

3 29 3 Weight Length Wheelbase 0.7065024 0.6966092 3.226956

4 30 3 EngineSize Weight Wheelbase 0.7045887 0.6946310 3.802229

5 31 3 Weight Width Wheelbase 0.7039881 0.6940102 3.982755

6 64 4 EngineSize Weight Length Wheelbase 0.7120588 0.6989706 3.556655

7 32 3 Weight Width Length 0.6974384 0.6872397 5.951620

8 65 4 Weight Width Length Wheelbase 0.7113915 0.6982729 3.757264

9 33 3 Weight Horsepower Wheelbase 0.6965448 0.6863160 6.220248

10 34 3 EngineSize Weight Length 0.6950183 0.6847380 6.679132

aic sbc

1 472.6393 482.7697

2 472.6919 482.8223

3 470.2133 482.8763

4 470.8178 483.4808

5 471.0066 483.6696

6 470.4358 485.6314

7 473.0419 485.7049

8 470.6511 485.8467

9 473.3162 485.9792

10 473.7829 486.4459

전진선택법

<- lm (MPG.highway~ 1 , data= dat93)step (model0, scope= ~ EngineSize+ Weight+ Price+ Width+ Length+ Horsepower+ Wheelbase, direction= "forward" )

Start: AIC=312.3

MPG.highway ~ 1

Df Sum of Sq RSS AIC

+ Weight 1 1718.70 896.62 214.74

+ Width 1 1072.43 1542.88 265.22

+ EngineSize 1 1027.48 1587.83 267.89

+ Horsepower 1 1002.23 1613.08 269.36

+ Wheelbase 1 990.41 1624.90 270.04

+ Price 1 822.16 1793.16 279.20

+ Length 1 770.83 1844.48 281.82

<none> 2615.31 312.30

Step: AIC=214.74

MPG.highway ~ Weight

Df Sum of Sq RSS AIC

+ Length 1 91.615 805.00 206.72

+ Wheelbase 1 91.160 805.46 206.77

+ Width 1 53.010 843.61 211.07

+ EngineSize 1 31.068 865.55 213.46

<none> 896.62 214.74

+ Price 1 5.845 890.77 216.13

+ Horsepower 1 2.334 894.28 216.50

Step: AIC=206.72

MPG.highway ~ Weight + Length

Df Sum of Sq RSS AIC

+ Wheelbase 1 37.413 767.59 204.29

<none> 805.00 206.72

+ Width 1 13.708 791.29 207.12

+ EngineSize 1 7.379 797.62 207.86

+ Price 1 4.135 800.87 208.24

+ Horsepower 1 0.207 804.79 208.69

Step: AIC=204.29

MPG.highway ~ Weight + Length + Wheelbase

Df Sum of Sq RSS AIC

<none> 767.59 204.29

+ EngineSize 1 14.5319 753.06 204.51

+ Width 1 12.7865 754.80 204.73

+ Horsepower 1 7.7950 759.79 205.34

+ Price 1 1.0351 766.55 206.16

Call:

lm(formula = MPG.highway ~ Weight + Length + Wheelbase, data = dat93)

Coefficients:

(Intercept) Weight Length Wheelbase

26.31687 -0.01107 0.08170 0.21005

후방제거

step (carfit, direction= "backward" )

Start: AIC=208.83

MPG.highway ~ EngineSize + Weight + Price + Width + Length +

Horsepower + Wheelbase

Df Sum of Sq RSS AIC

- Width 1 1.06 740.58 206.96

- EngineSize 1 4.18 743.69 207.35

- Price 1 5.47 744.98 207.51

- Horsepower 1 8.51 748.02 207.89

- Length 1 16.01 755.52 208.82

<none> 739.51 208.82

- Wheelbase 1 48.00 787.51 212.67

- Weight 1 480.82 1220.33 253.41

Step: AIC=206.96

MPG.highway ~ EngineSize + Weight + Price + Length + Horsepower +

Wheelbase

Df Sum of Sq RSS AIC

- EngineSize 1 7.73 748.31 205.93

- Price 1 9.67 750.25 206.17

- Horsepower 1 10.29 750.87 206.24

<none> 740.58 206.96

- Length 1 19.54 760.12 207.38

- Wheelbase 1 51.04 791.62 211.16

- Weight 1 514.25 1254.83 254.00

Step: AIC=205.93

MPG.highway ~ Weight + Price + Length + Horsepower + Wheelbase

Df Sum of Sq RSS AIC

- Price 1 11.48 759.79 205.34

<none> 748.31 205.93

- Horsepower 1 18.24 766.55 206.16

- Length 1 32.26 780.57 207.85

- Wheelbase 1 51.62 799.93 210.13

- Weight 1 516.55 1264.86 252.74

Step: AIC=205.34

MPG.highway ~ Weight + Length + Horsepower + Wheelbase

Df Sum of Sq RSS AIC

- Horsepower 1 7.79 767.59 204.29

<none> 759.79 205.34

- Length 1 33.84 793.63 207.39

- Wheelbase 1 45.00 804.79 208.69

- Weight 1 508.94 1268.73 251.03

Step: AIC=204.29

MPG.highway ~ Weight + Length + Wheelbase

Df Sum of Sq RSS AIC

<none> 767.59 204.29

- Wheelbase 1 37.41 805.00 206.72

- Length 1 37.87 805.46 206.77

- Weight 1 846.75 1614.34 271.43

Call:

lm(formula = MPG.highway ~ Weight + Length + Wheelbase, data = dat93)

Coefficients:

(Intercept) Weight Length Wheelbase

26.31687 -0.01107 0.08170 0.21005

단계별 선택

<- lm (MPG.highway~ 1 , data= dat93)step (model0, scope= ~ EngineSize+ Weight+ Price+ Width+ Length+ Horsepower+ Wheelbase, direction= "both" )

Start: AIC=312.3

MPG.highway ~ 1

Df Sum of Sq RSS AIC

+ Weight 1 1718.70 896.62 214.74

+ Width 1 1072.43 1542.88 265.22

+ EngineSize 1 1027.48 1587.83 267.89

+ Horsepower 1 1002.23 1613.08 269.36

+ Wheelbase 1 990.41 1624.90 270.04

+ Price 1 822.16 1793.16 279.20

+ Length 1 770.83 1844.48 281.82

<none> 2615.31 312.30

Step: AIC=214.74

MPG.highway ~ Weight

Df Sum of Sq RSS AIC

+ Length 1 91.62 805.00 206.72

+ Wheelbase 1 91.16 805.46 206.77

+ Width 1 53.01 843.61 211.07

+ EngineSize 1 31.07 865.55 213.46

<none> 896.62 214.74

+ Price 1 5.85 890.77 216.13

+ Horsepower 1 2.33 894.28 216.50

- Weight 1 1718.70 2615.31 312.30

Step: AIC=206.72

MPG.highway ~ Weight + Length

Df Sum of Sq RSS AIC

+ Wheelbase 1 37.41 767.59 204.29

<none> 805.00 206.72

+ Width 1 13.71 791.29 207.12

+ EngineSize 1 7.38 797.62 207.86

+ Price 1 4.14 800.87 208.24

+ Horsepower 1 0.21 804.79 208.69

- Length 1 91.62 896.62 214.74

- Weight 1 1039.48 1844.48 281.82

Step: AIC=204.29

MPG.highway ~ Weight + Length + Wheelbase

Df Sum of Sq RSS AIC

<none> 767.59 204.29

+ EngineSize 1 14.53 753.06 204.51

+ Width 1 12.79 754.80 204.73

+ Horsepower 1 7.79 759.79 205.34

+ Price 1 1.04 766.55 206.16

- Wheelbase 1 37.41 805.00 206.72

- Length 1 37.87 805.46 206.77

- Weight 1 846.75 1614.34 271.43

Call:

lm(formula = MPG.highway ~ Weight + Length + Wheelbase, data = dat93)

Coefficients:

(Intercept) Weight Length Wheelbase

26.31687 -0.01107 0.08170 0.21005

ols_step_forward_aic (carfit, details = TRUE )

Forward Selection Method

------------------------

Candidate Terms:

1. EngineSize

2. Weight

3. Price

4. Width

5. Length

6. Horsepower

7. Wheelbase

Step => 0

Model => MPG.highway ~ 1

AIC => 578.2207

Initiating stepwise selection...

Table: Adding New Variables

-----------------------------------------------------------------------

Predictor DF AIC SBC SBIC R2 Adj. R2

-----------------------------------------------------------------------

Weight 1 480.663 488.261 216.331 0.65717 0.65340

Width 1 531.141 538.739 264.864 0.41006 0.40358

EngineSize 1 533.812 541.410 267.447 0.39287 0.38620

Horsepower 1 535.280 542.878 268.867 0.38322 0.37644

Wheelbase 1 535.959 543.556 269.524 0.37870 0.37187

Price 1 545.122 552.720 278.402 0.31436 0.30683

Length 1 547.746 555.344 280.948 0.29474 0.28699

-----------------------------------------------------------------------

Step => 1

Added => Weight

Model => MPG.highway ~ Weight

AIC => 480.6632

Table: Adding New Variables

-----------------------------------------------------------------------

Predictor DF AIC SBC SBIC R2 Adj. R2

-----------------------------------------------------------------------

Length 1 472.639 482.770 208.747 0.69220 0.68536

Wheelbase 1 472.692 482.822 208.797 0.69202 0.68518

Width 1 476.996 487.126 212.824 0.67744 0.67027

EngineSize 1 479.384 489.514 215.061 0.66905 0.66169

Price 1 482.055 492.185 217.566 0.65940 0.65183

Horsepower 1 482.421 492.551 217.909 0.65806 0.65046

-----------------------------------------------------------------------

Step => 2

Added => Length

Model => MPG.highway ~ Weight + Length

AIC => 472.6393

Table: Adding New Variables

-----------------------------------------------------------------------

Predictor DF AIC SBC SBIC R2 Adj. R2

-----------------------------------------------------------------------

Wheelbase 1 470.213 482.876 206.718 0.70650 0.69661

Width 1 473.042 485.705 209.299 0.69744 0.68724

EngineSize 1 473.783 486.446 209.975 0.69502 0.68474

Price 1 474.160 486.823 210.320 0.69378 0.68346

Horsepower 1 474.615 487.278 210.736 0.69228 0.68190

-----------------------------------------------------------------------

Step => 3

Added => Wheelbase

Model => MPG.highway ~ Weight + Length + Wheelbase

AIC => 470.2133

Table: Adding New Variables

-----------------------------------------------------------------------

Predictor DF AIC SBC SBIC R2 Adj. R2

-----------------------------------------------------------------------

EngineSize 1 470.436 485.631 207.247 0.71206 0.69897

Width 1 470.651 485.847 207.438 0.71139 0.69827

Horsepower 1 471.264 486.460 207.982 0.70948 0.69628

Price 1 472.088 487.283 208.714 0.70690 0.69358

-----------------------------------------------------------------------

No more variables to be added.

Variables Selected:

=> Weight

=> Length

=> Wheelbase

Stepwise Summary

-------------------------------------------------------------------------

Step Variable AIC SBC SBIC R2 Adj. R2

-------------------------------------------------------------------------

0 Base Model 578.221 583.286 311.963 0.00000 0.00000

1 Weight 480.663 488.261 216.331 0.65717 0.65340

2 Length 472.639 482.770 208.747 0.69220 0.68536

3 Wheelbase 470.213 482.876 206.718 0.70650 0.69661

-------------------------------------------------------------------------

Final Model Output

------------------

Model Summary

---------------------------------------------------------------

R 0.841 RMSE 2.873

R-Squared 0.707 MSE 8.254

Adj. R-Squared 0.697 Coef. Var 10.097

Pred R-Squared 0.665 AIC 470.213

MAE 2.139 SBC 482.876

---------------------------------------------------------------

RMSE: Root Mean Square Error

MSE: Mean Square Error

MAE: Mean Absolute Error

AIC: Akaike Information Criteria

SBC: Schwarz Bayesian Criteria

ANOVA

--------------------------------------------------------------------

Sum of

Squares DF Mean Square F Sig.

--------------------------------------------------------------------

Regression 1847.724 3 615.908 71.413 0.0000

Residual 767.588 89 8.625

Total 2615.312 92

--------------------------------------------------------------------

Parameter Estimates

----------------------------------------------------------------------------------------

model Beta Std. Error Std. Beta t Sig lower upper

----------------------------------------------------------------------------------------

(Intercept) 26.317 7.088 3.713 0.000 12.233 40.401

Weight -0.011 0.001 -1.225 -9.909 0.000 -0.013 -0.009

Length 0.082 0.039 0.224 2.095 0.039 0.004 0.159

Wheelbase 0.210 0.101 0.269 2.083 0.040 0.010 0.410

----------------------------------------------------------------------------------------

ols_step_forward_p (carfit, details = TRUE )

Forward Selection Method

------------------------

Candidate Terms:

1. EngineSize

2. Weight

3. Price

4. Width

5. Length

6. Horsepower

7. Wheelbase

Step => 0

Model => MPG.highway ~ 1

R2 => 0

Initiating stepwise selection...

Selection Metrics Table

----------------------------------------------------------------

Predictor Pr(>|t|) R-Squared Adj. R-Squared AIC

----------------------------------------------------------------

Weight 0.00000 0.657 0.653 480.663

Width 0.00000 0.410 0.404 531.141

EngineSize 0.00000 0.393 0.386 533.812

Horsepower 0.00000 0.383 0.376 535.280

Wheelbase 0.00000 0.379 0.372 535.959

Price 0.00000 0.314 0.307 545.122

Length 0.00000 0.295 0.287 547.746

----------------------------------------------------------------

Step => 1

Selected => Weight

Model => MPG.highway ~ Weight

R2 => 0.657

Selection Metrics Table

----------------------------------------------------------------

Predictor Pr(>|t|) R-Squared Adj. R-Squared AIC

----------------------------------------------------------------

Length 0.00190 0.692 0.685 472.639

Wheelbase 0.00195 0.692 0.685 472.692

Width 0.01952 0.677 0.670 476.996

EngineSize 0.07563 0.669 0.662 479.384

Price 0.44422 0.659 0.652 482.055

Horsepower 0.62912 0.658 0.650 482.421

----------------------------------------------------------------

Step => 2

Selected => Length

Model => MPG.highway ~ Weight + Length

R2 => 0.692

Selection Metrics Table

----------------------------------------------------------------

Predictor Pr(>|t|) R-Squared Adj. R-Squared AIC

----------------------------------------------------------------

Wheelbase 0.04014 0.707 0.697 470.213

Width 0.21761 0.697 0.687 473.042

EngineSize 0.36665 0.695 0.685 473.783

Price 0.49960 0.694 0.683 474.160

Horsepower 0.88015 0.692 0.682 474.615

----------------------------------------------------------------

Step => 3

Selected => Wheelbase

Model => MPG.highway ~ Weight + Length + Wheelbase

R2 => 0.707

Selection Metrics Table

----------------------------------------------------------------

Predictor Pr(>|t|) R-Squared Adj. R-Squared AIC

----------------------------------------------------------------

EngineSize 0.19593 0.712 0.699 470.436

Width 0.22536 0.711 0.698 470.651

Horsepower 0.34463 0.709 0.696 471.264

Price 0.73113 0.707 0.694 472.088

----------------------------------------------------------------

Step => 4

Selected => EngineSize

Model => MPG.highway ~ Weight + Length + Wheelbase + EngineSize

R2 => 0.712

Selection Metrics Table

----------------------------------------------------------------

Predictor Pr(>|t|) R-Squared Adj. R-Squared AIC

----------------------------------------------------------------

Width 0.46764 0.714 0.697 471.869

Horsepower 0.56977 0.713 0.697 472.088

Price 0.61570 0.713 0.696 472.165

----------------------------------------------------------------

No more variables to be added.

Variables Selected:

=> Weight

=> Length

=> Wheelbase

=> EngineSize

Stepwise Summary

-------------------------------------------------------------------------

Step Variable AIC SBC SBIC R2 Adj. R2

-------------------------------------------------------------------------

0 Base Model 578.221 583.286 311.963 0.00000 0.00000

1 Weight 480.663 488.261 216.331 0.65717 0.65340

2 Length 472.639 482.770 208.747 0.69220 0.68536

3 Wheelbase 470.213 482.876 206.718 0.70650 0.69661

4 EngineSize 470.436 485.631 207.247 0.71206 0.69897

-------------------------------------------------------------------------

Final Model Output

------------------

Model Summary

---------------------------------------------------------------

R 0.844 RMSE 2.846

R-Squared 0.712 MSE 8.097

Adj. R-Squared 0.699 Coef. Var 10.057

Pred R-Squared 0.664 AIC 470.436

MAE 2.081 SBC 485.631

---------------------------------------------------------------

RMSE: Root Mean Square Error

MSE: Mean Square Error

MAE: Mean Absolute Error

AIC: Akaike Information Criteria

SBC: Schwarz Bayesian Criteria

ANOVA

--------------------------------------------------------------------

Sum of

Squares DF Mean Square F Sig.

--------------------------------------------------------------------

Regression 1862.256 4 465.564 54.404 0.0000

Residual 753.056 88 8.557

Total 2615.312 92

--------------------------------------------------------------------

Parameter Estimates

----------------------------------------------------------------------------------------

model Beta Std. Error Std. Beta t Sig lower upper

----------------------------------------------------------------------------------------

(Intercept) 28.439 7.246 3.925 0.000 14.040 42.839

Weight -0.012 0.001 -1.334 -8.960 0.000 -0.015 -0.009

Length 0.063 0.041 0.172 1.511 0.134 -0.020 0.145

Wheelbase 0.233 0.102 0.298 2.282 0.025 0.030 0.435

EngineSize 0.766 0.587 0.149 1.303 0.196 -0.402 1.933

----------------------------------------------------------------------------------------

연습문제 6.12

set.seed (13111 )<- 10 <- 50 <- 100 <- (num_of_ind_var+ 1 )* n<- matrix (rnorm (N), ncol= num_of_ind_var+ 1 )<- data.frame (randata)<- names (randata)[1 : 50 ]<- NULL <- NULL <- NULL <- NULL for (i in 1 : Nsim) {<- matrix (rnorm (N), ncol= num_of_ind_var+ 1 )<- data.frame (randata)# === 함수 step(..direction="backward")는 AIC 를 이용 <- lm (X51 ~ ., data= randata)<- step (fit.lm, direction= "backward" , trace= 0 )<- as.character (attr (res$ terms, "variables" ))[- c (1 ,2 )]# ==== 함수 step(...direction = "forward"..) 은 AIC 를 이용 # fit.null <- lm(X51 ~ 1, data=randata) # res <- step(fit.null, scope~ X1 + X2 + X3 + X4 + X5 + X6 + X7 + X8 + X9 + X10 + X11 + X12 + # X13 + X14 + X15 + X16 + X17 + X18 + X19 + X20 + X21 + X22 + # X23 + X24 + X25 + X26 + X27 + X28 + X29 + X30 + X31 + X32 + # X33 + X34 + X35 + X36 + X37 + X38 + X39 + X40 + X41 + X42 + # X43 + X44 + X45 + X46 + X47 + X48 + X49 + X50 , direction = "forward", trace=0) # ariable.entered <- as.character(attr(res$terms, "variables"))[-c(1,2)] # === 함수 ols_step_backward_p 는 F-검정을 이용 # fit.lm <- lm(X51 ~ ., data=randata) # aa <- ols_step_backward_p(fit.lm) # variable.entered <- names(aa$model$coefficients)[-1] # === 함수 ols_step_forward_p 는 F-검정을 이용 # fit.lm <- lm(X51 ~ ., data=randata) # aa <- ols_step_forward_p(fit.lm) # variable.entered <- names(aa$model$coefficients)[-1] <- c (variables.set, variable.entered )<- c (p, length (variable.entered))<- c ( r2.set , summary (res)$ r.squared)<- c ( r2adj.set , summary (res)$ adj.r.squared)<- factor (variables.set, levels= indvarname)table (variables.set)

variables.set

X1 X2 X3 X4 X5 X6 X7 X8 X9 X10 X11 X12 X13 X14 X15 X16 X17 X18 X19 X20

2 3 3 3 2 5 5 1 5 0 3 4 0 4 2 4 3 2 1 2

X21 X22 X23 X24 X25 X26 X27 X28 X29 X30 X31 X32 X33 X34 X35 X36 X37 X38 X39 X40

6 3 4 2 4 4 3 1 4 3 2 3 2 1 3 4 2 1 2 5

X41 X42 X43 X44 X45 X46 X47 X48 X49 X50

2 2 3 2 2 3 1 2 4 0

Min. 1st Qu. Median Mean 3rd Qu. Max.

7.0 9.0 14.0 13.4 17.0 20.0

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.2228 0.2909 0.3612 0.3570 0.4050 0.5094

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.1545 0.2094 0.2635 0.2595 0.2938 0.3852